In this blog UKERC revisits options for breaking the link between gas and electricity prices in the light of the impact of the US-led attacks on Iran.

When the United States launched ‘Epic Fury’ on 28 February 2026 the impact on UK gas prices was significant but initially muted in comparison to the Ukraine crisis. Over the first 5 days of the conflict prices increased from around 80 pence per therm to over 150 pence before dropping back a little. By contrast, when Russia invaded Ukraine on 24 February 2022 prices spiked at over 400 pence per therm within 4 days – although prices were already elevated due to post-Covid shortfalls.

Futures markets moved even less at first, indicating market expectations of a short war, with relatively limited impact on gas supplies to the UK. The loss of Qatar’s Ras Laffan facility, the world’s largest LNG plant, changed matters, with spot prices spiking to around 170 pence per therm, and UK gas futures for 2027 showing around 120 pence per therm on the 19th March. Spot prices for gas fell back to around 140 pence per therm, after Donald Trump announced a five day pause on US strikes against Iranian energy infrastructure following discussions aimed at ending the conflict. Uncertainty created by such announcement-driven pricing seems to be reducing volumes of forward trading in the GB gas market, making it harder to glean information about market expectations on future gas prices.

British consumers (domestic consumers at least) are protected from the price shocks until June by the Ofgem price cap. But indications are that Autumn bills could rise by around 20% relative to the April cap as the raised prices feed through. Predicting prices beyond that becomes difficult in the absence of liquid futures markets.

First and foremost, this is a gas price issue. Unfortunately, interventions that could effectively target gas prices are not obvious. They are set through international regional markets and largely outside the control of individual countries, at least in the absence of a move back to long-term state-backed contracts. As UKERC Researchers have argued elsewhere, the debate over new licenses in the North Sea is a red herring, since new extraction in the UK continental shelf (UKCS) will take years and will not have a material impact on UK oil or gas prices. However, the way that the electricity market operates in Britain means that there is a knock-on impact from gas price volatility on power prices. Policymakers paid attention to breaking this link in 2022/23 during the height of the Ukraine war-induced price crisis. Unfortunately, as yet no specific action has been taken to change the way that the electricity market operates, so electricity prices still follow gas prices upwards.

It is important to keep the current situation in proportion. The impact on UK wholesale power prices is significant, but at around £110/MWh compared to a pre-crisis level of £75/MWh we are a long way from the £500+/MWh peaks of the Ukraine crisis in 2023. Nevertheless, the crisis is extremely uncertain, prices now reflect seasonal factors and may be a poor guide to the future. Recent events give the lie to confident predictions of low oil and gas prices and we have a bit of time to consider how to insulate power prices from any future gas price spikes before the winter. It will not help with petrol or gas heating, but since the UK already secures 68% of its electricity from a mix of nuclear and renewables it is reasonable to ask why the price of electricity at least, a key component of household expenditure and inflation measures, can’t be divorced from this unfolding and unpredictable geopolitical crisis – and those that follow.

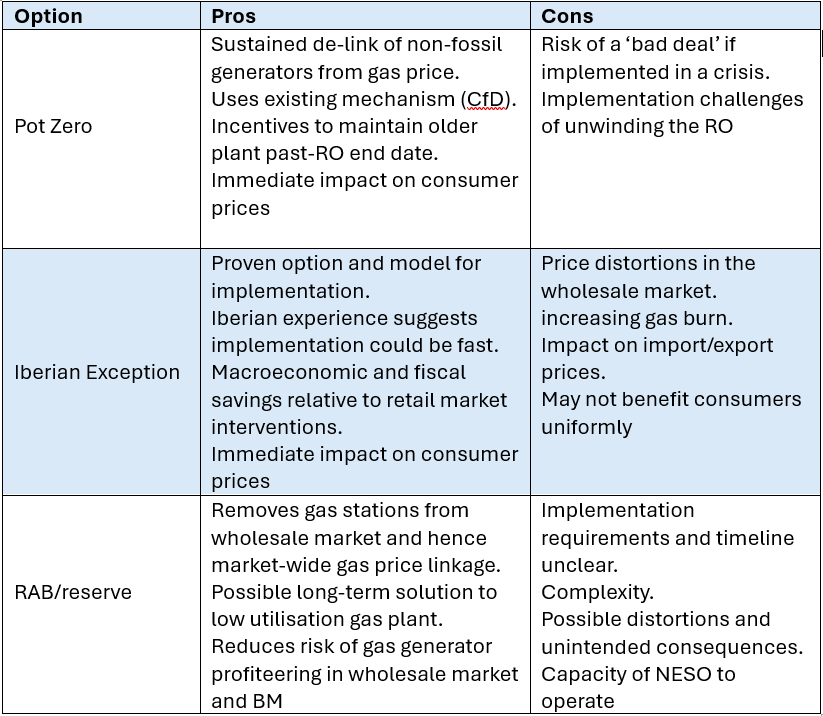

In April 2022 UKERC published our first paper on a ‘Pot Zero’ contract for difference (CfD) for legacy renewable and nuclear plants. Our objective then was to provide a practical and implementable proposal to reduce electricity prices in the face of the Ukraine war. Pot Zero is also a means to delink power and gas prices, by putting a larger share of total generation under a long-run fixed price that is independent of global gas prices. Our analysis then pointed to a prospective saving of up to £22bn, or £300 per household, based on 2022’s sky high wholesale gas and power prices.

Updated analysis undertaken in 2025 and prior to the upswing in gas prices pointed to savings ranging between £2bn and £8bn per year, depending on relative CfD and wholesale power prices. The recent increase in prices adds a further £1.5-2.5bn per year to these savings for as long as the high prices persist. Recent events demonstrate yet again the vulnerability of fossil fuel prices to geopolitical events that are hard or impossible to guess. In our 2025 update we included a ‘high’ gas price scenario that is already out of date, and around 40 pence per therm below the current spot price.

Pot zero offers a number of benefits: (i) it could reduce prices for all consumers (including commercial customers), (ii) reduce the costs to the Treasury of the RO rebate announced in last year’s budget, (iii) go beyond the RO rebate by delivering electricity below prevailing wholesale prices, (iv) ensure serviceable renewable power stays online for longer, and (v) help make power prices less volatile in future. Perhaps the savings to the Treasury could be used to socialise other policy costs currently recovered from electricity bills and allow for further cuts to consumer prices.

The lower the strike price achieved, more quickly Pot Zero is implemented, and wider the participation, the greater the benefits during another period of instability and high prices. For all these reasons, Pot Zero offers a useful approach to stabilising power prices and delinking them from gas, and that the current situation gives a fresh imperative for considering implementation urgently. We understand the concern expressed to us by several stakeholders that implementing pot zero in a crisis risks a ‘bad deal’, with Pot Zero strike price set too high. Indeed, we understand that is one of the reasons it was not implemented during the Ukraine crisis. It is extremely unfortunate that the idea was not pursued during more benign times, when presumably a ‘good deal’ might have been struck.

It seems reasonable to proceed on the basis that it would not make sense to implement a Pot Zero type policy unless it can be done on a cost-effective basis that would not lead to regret once the crisis has passed. There is no reason to assume that a bad deal is inevitable, since government would not need to commit to any pot zero CfDs should their price appear too high. Pot zero also has a range of variations, one being to limit the CfD component to the wholesale price, leaving the RO payment in place (so called wholesale price CfD). This could potentially be implemented more quickly.

Before dispensing with the concept on the basis that a price crisis is the wrong time to implement, policymakers could explore the art of the possible and try to ensure a positive outcome, both as a crisis response and longer-term solution. Nevertheless, there are other options; indeed, the objective of this article is to explore a range of options to delink power prices from gas. The first alternative we consider is a temporary price cap on gas, with a subsidy to gas generators, as implemented in the Ukraine crisis by Spain and Portugal.

The Iberian Exception was a temporary, emergency market intervention approved by the European Commission in June 2022. It allowed Spain and Portugal to decouple the price of electricity from natural gas prices during the energy crisis that followed Russia’s invasion of Ukraine. The mechanism introduced a price ceiling on natural gas used by power stations. It started at €40 per megawatt-hour (MWh) in June 2022 and gradually increased on a monthly basis to €65/MWh by the end of the scheme in 2023. Gas plant operators had to buy gas at European market rates, which were much higher than the cap. To prevent them from going bankrupt, they were compensated for the difference between the actual gas price and the cap.

This compensation was funded by a surcharge levied on all electricity consumers, making the intervention revenue neutral for the Spanish and Portuguese governments, whilst holding down prices market-wide. It is worth pausing for a moment to understand how this is possible. By capping the price that gas generators were allowed to bid, the average price for the whole market was reduced, including the price paid to coal, renewable and nuclear power stations. This works when there is a big difference between the proportion of gas on the system and the volume of generation for which revenues are driven by the marginal price of gas generation. Gas provided around 20% of total generation in Spain and Portugal in 2022, so the consumer levy only had to pay for the price cap-subsidy on the portion of total generation from gas plant.

This contrasts with the UK experience, which largely intervened in the retail market, by capping the price that suppliers could pass through to domestic consumers and subsidising suppliers, rather than gas-fired generators[i]. This approach required a subsidy to the whole market, not just to gas generators. It resulted in very significant public expenditure, estimated at around £40bn, that has contributed to the current fiscal difficulties faced by the UK. The Iberian exception appears to have cost around €8bn, and was levy funded, so did not increase public spending.

The Iberian exception worked to delink Iberian wholesale power prices from the ongoing gas price crisis and held down consumer prices and inflation. There is debate over how effective the approach was at holding down prices for all consumers, given the interacting effects of the levy, wholesale price, and pre-existing measures to protect consumers. The intervention led to an increase in exports to France (which was suffering from nuclear outages) and North Africa, with consequential cross subsidy from consumers in Iberia to neighbouring countries. It increased gas burn relative to what might have happened without the cap, by changing the relative economics of gas, coal, hydro and exports, though low rainfall also affected hydro plants. Subsidising gas power in this way had the perverse impact of increasing gas burn at a time when gas was expensive.

Several studies have highlighted the micro-economic shortcomings of the Iberian exception. Clearly, increasing gas burn during a gas price crisis represents a significant inefficiency. However, we have not found any analysis of the macro-economic impact of the Iberian policy – on inflation, interest rates, public borrowing and growth – relative to the approach taken by the UK (and others) where the wholesale market was left unchecked, with intervention in retail markets to protect households or industry.

It is possible that viewed through a macro-economic lens, the Iberian policy was a success, and the inevitable inefficiencies of intervening in the wholesale market a price worth paying for societal and macro-economic benefits. In comparison to the UK experience, with a broadly comparable mix of gas and renewables, the intervention would appear to have been a lot cheaper. UK Treasury expenditure in the form of retail subsidies was largely avoided, and the mechanism helped Spain and Portugal maintain some of the lowest inflation rates in the Eurozone during late 2022 and early 2023. The UK approach also helped to hold down inflation but because it allowed market-wide power prices to increase significantly, it was inevitable that the intervention was more expensive.

Under the Iberian exception, a levy was used to subsidise the cost of gas and push the wholesale price of power down. Gas generators were still paid more than renewables, nuclear and the rest, and consumers still paid for the gas. With Pot Zero, or any approach that targets the price paid to renewable and other non-gas generators, the outcome is in some respects quite similar. Highly priced gas generation still runs and is still paid for by consumers, and the rest of the market is still paid a lower price. The differences are structural: With the Iberian exception an out-of-market support mechanism made up for a shortfall in gas purchase price. With Pot Zero a market intervention effectively removes renewable (and possibly nuclear) from the wholesale market[ii].

In the context of a crisis the questions that appear pertinent are how fast either approach can be implemented, what the downsides are, and how material they could be in reducing prices. In the current context, where a market-wide bailout of households through public spending appears fiscally impossible, both approaches deserve careful consideration. To oversimplify somewhat, as a crisis-only intervention the Iberian model might have merits despite the inevitable distortions and inefficiencies created by intervening in the wholesale market (and with potential to reduce such distortions through improved interconnector re-dispatch options being considered under Reformed National Pricing). Pot Zero would appear to offer a similar outcome through a more structural route, with fewer market distortions, but perhaps more regulatory impediments to implementation. It offers the benefit of a long-term de-link from gas prices for much of the power market, but the risk of a bad deal that sustains once the crisis is over. We therefore consider a third option, that seeks to remove gas-fired power stations from the wholesale market altogether.

The Iberian exception was just that, an exceptional intervention born of exceptional circumstances, time limited and withdrawn once the most dramatic impacts of the Ukraine war on gas price receded. Few people would advocate for ongoing subsidies to gas fired power stations. Perhaps more long term, other options include removing gas power stations from the wholesale market altogether – by moving them into a strategic reserve – and/or changing the way gas power stations are owned and remunerated. Since a variety of proposals have been mooted (example from Greenpeace, Stonehaven and Common-wealth), we simplify here to two interrelated but distinct changes: placing gas on a RAB model, and making gas power stations into a strategic reserve, centrally dispatched by the system operator (NESO).

Current GB power market arrangements date back to the early 2000s and are predicated on power generation operating as a competitive market through which generators and suppliers can trade electricity directly. A central tenet of the approach is that as generators participate in a competitive market there is no requirement for government intervention to cap their returns on investment. Any company making excessive profits at the expense of consumers would expect to be challenged by new entrants, competing away their excess profits. This contrasts with network companies, which operate in a natural monopoly where competition is impossible or inefficient. Network companies are therefore ‘regulated assets’, and Ofgem operates a sophisticated framework to ensure that their profits are fair and reflect necessary investment or innovation that is in the interest of consumers.

Some years ago, when gas, nuclear and coal generation dominated the supply of electricity in Britain, this arrangement appeared to work well, with generators remunerated through a combination of wholesale market revenues, Balancing Mechanism (BM) revenues and (since 2014) Capacity Market (CM) payments. However, the argument is that as gas power stations run at ever lower load factors due to the rising capacity of renewables it is increasingly necessary to make larger payments through the CM, and a diminishing number of gas generators can exercise considerable market power when the supply of renewable power is low and demand is high – whether purchased through the wholesale market or in the BM. Therefore, it would be cheaper to take the gas power stations out of the wholesale market, CM and BM, and treat them more like network assets. Doing so could be achieved by placing them on a RAB model, where they stay in private ownership and the profits of gas power station owners are regulated – as they are for power and gas network assets.

In principle it is possible to put in place a RAB to control the behaviour of gas fired generators without removing them from the wholesale market. This would make sense if policymakers believe that gas generators are making excess profits in the BM or wholesale market, for which there is some evidence. RAB only generators would be obliged to do cost plus pricing, and so only ever bid in on the basis of marginal cost.

However, for most commentators on the topic the RAB approach brings with it an important corollary, which is that rather than relying on the wholesale market to determine the demand for gas-fired power, NESO should put in place contracts for ‘strategic reserve’ and centrally dispatch gas fired power stations when they are needed. A similar model is used for storage and other assets that provide response and reserve services. Viewed from the perspective of delinking gas and power prices, the advantage of this approach is that the current situation where wholesale power market prices market wide are usually set by gas could be eliminated. Instead, wholesale prices would reflect demand and supply imbalances, and a mix of demand side response and storage could help keep the power system in balance – with the strategic reserve only deployed when needed. It has also been suggested that NESO could act as a central buyer of gas (as fuel for power stations), doing so through long term contracts that might be able to mitigate short-term price shocks.

Critics of the approach question the capacity of NESO to effectively ‘police’ the utilisation of gas assets, act as a buyer of gas, and the need for implementation now, when gas still provides around a third of total electricity. The approach is largely unproven internationally, and it is not clear what the implementation challenges might amount to – in terms of regulatory change, market arrangements and compensation needs, NESO capabilities and so on. Proponents argue that it could be delivered through a simple change to Ofgem licence conditions, and if this is correct the implementation challenges would be minor.

Another criticism is that the strategic reserve and wholesale market would interact, with market participants aware of the cost of dispatching the reserve and pricing accordingly. Unless the system operator dispatched the reserve at below market price it seems that there would be scope for distortions that could diminish the value of the reserve as a means to reduce wholesale price – or for a subsidy to gas generators that appears to be similar to the Iberian approach. Either way, market distortions and interactions would need to be evaluated.

As a long-term structural change that deals with the declining load factors of gas-fired power stations the combination of a strategic reserve and gas-RAB model has considerable merit, and it is in this context that the idea was first mooted (although recently it has been promoted as a delinking mechanism). As a crisis response measure the approach could work, but only if it can be implemented quickly. If the idea is to be taken forward the implementation requirements need to be investigated urgently. Pot Zero was examined in detail during the previous crisis and uses an established mechanism (the CfD), and the Iberian Exception was implemented in practice in a broadly similar wholesale electricity market context. If proponents are right that the RAB/single buyer model can be implemented easily, and fast, then it meets the principal requirement of crisis intervention. If not, then it is better considered as a longer term shift that brings other benefits.

Table 1 provides an overview of the pros and cons of the options reviewed above. Further action is needed to assess each option in more detail.

The approach that the UK government is de facto already pursuing is to rely on ongoing efforts to accelerate the deployment of renewables to reduce the role of gas as a price setter. Since the share of renewables with a CfD is steadily rising each year, within a few more years the volume of capacity with a fixed price contract will have increased significantly. Previous analysis by UKERC has reviewed the impact of this on price formation, noting gas-linked revenues are set to decline significantly by the late 2020s. Alongside other changes to the generation mix and market this could lower average prices by £7/MWh and save consumers around £20 annually – based on 2025, pre- Epic Fury wholesale prices. This modest impact reflects the relative similarity of CfD and wholesale prices, and the differential will widen if higher gas prices become the norm. It remains to be seen whether government is content to wait it out, rather than intervene now to actively break the gas-to-power price relationship.

Government took action on some policy costs in the Autumn Budget and it would be possible to consider further action to remove levies from electricity bills. Carbon pricing has attracted particular attention in recent debates. The prices bid by gas-fired power stations in the GB market are a function of both the gas price and the carbon price. The latter is a product of the Carbon Price Support (CPS) mechanism, a tax introduced in 2014, and the GB Emissions Trading Scheme (ETS). These have a combined impact of about £20/MWh on gas power station prices. This is broadly similar to the upswing in the wholesale power price since the start of Epic Fury and a temporary tax reduction is worthy of consideration as a crisis measure to help alleviate the impact on consumers.

However, removing carbon prices would offer very limited effect were wholesale prices to return to the levels experienced in 2022/2023, when wholesale prices were elevated far above current levels and peaked at close to £600/MWh. The UK is currently negotiating reintegrating with the European integrated electricity market or IEM, which also operates an ETS. Perhaps only the CPS element, worth around £7/MWh, could be removed without complicating these negotiations. Carbon pricing alone is not a game changer. This does not mean it should not be considered as part of a package of emergency measures that include fiscal and policy cost derogations.

Action on policy costs does not actively delink gas and power prices, it simply reduces the overall price of electricity by removing some of the costs borne by consumers. This is an important possible policy response to the crisis, but separate from, and may be implemented alongside, action to delink gas and power prices.

Similar considerations pertain to windfall taxes on energy producers via the energy profits levy (EPL, on oil and gas extraction) and the electricity generator levy (EGL, on non-fossil electricity generators). The latter offers the potential to reduce excess profits made by non-fossil generators during times of elevated fuel prices. In principle the government could redistribute funds from non-fossil generators to households and businesses, if hypothecated either directly via suppliers or indirectly to target vulnerable households. The £6bn revenue of the EGL and EPL (of which 80% originated from the EPL), did not come close to the level of 2022/23 EPG bailout. But the EGL could serve alongside other measures, for example as a temporary intervention using existing mechanisms, to allow time for Pot Zero implementation.

The government has also signalled that it will focus support on need rather than market wide. This is perfectly understandable given the UK’s fiscal situation and the high fiscal costs incurred during 2022 and 2023. However, this does not mean that the value of interventions that reduce the overall scale of the problem should be discounted, and it is essential that the root of the problem is understood. The wholesale market we have had in place for 25 years may no longer be fit for purpose, irrespective of price crises. Indeed, this is why successive governments spent 3 years debating market reforms through the REMA process. Price crises exacerbate the problem, and resolving it is a matter of high national significance. It is not resolved through retail market patch up measures, whether they are targeted to vulnerable consumers or otherwise.

Ultimately it is not possible to divorce action to delink gas and power prices from ongoing efforts to reduce electricity prices, even before the impact of the war on Iran. Consumer prices are a function of each component of the Ofgem price cap stack – from the cost of generation, need for and financing of network build, efficiency of wholesale and retail markets, and policy costs. This is reflected in UKERC’s Mission on Bills, which is looking at options across the whole chain. But gas prices continue to be a core driver of power prices, so action on the gas-to-power price link is fundamentally important.

The end goal for the UK has to be to create an electricity system and market that provides affordable and predictable prices, based on the resource base that the UK has access to, and which provides a basis for electrification of heating and transport. Like a fixed-price mortgage, a stable electricity price would offer households and businesses an element of certainty in an uncertain world. The more we can electrify our economy, the greater economic and social benefit such stability would provide.

Other countries such as Canada, Norway and France show what is possible. With their largely low carbon, renewable and nuclear systems, power prices are both low and relatively insulated to global disruptions[iii]. Last year’s CfD auction results delivered contracts for wind and solar schemes well below current wholesale prices. Only in a low gas price future would renewable energy turn out to be more expensive than gas, and the current situation demonstrates how uncertain that is. Price shocks may once have been occasional mishaps in a broadly functional globalised context. They may now be endemic to an era of regionalisation and conflict.

Despite recent experience with events in Ukraine, UK energy policy debates prior to the Iran crisis apparently drifted back to an implicit assumption that fossil prices are stable and predictable. This collective amnesia could return when the current crisis passes. If this is to be avoided, action during the crisis needs to pave the way for changes that sustain after it has passed.

Delinking power and gas price is possible. The changes needed aren’t simple, because electricity markets are not simple. Complexity is not a reason for inaction. Action needs to start by evaluating crisis response measures, with a primary criterion being speedy implementation if needed in time for next winter, and with macroeconomic and societal impacts evaluated alongside, and perhaps with priority over, microeconomic concerns. Building on this, we need immediate evaluation of enduring options to ensure electricity prices are as stable and robust to gas-price spikes as possible.

[i] We include here the Energy Price Guarantee and Energy Bills Support Scheme, for households, and Energy Bills Relief Scheme, for business. We do not include the Council Tax rebate or means tested payments to some households, or the cost of bailing out failed suppliers. Outturn data from OBR.

[ii] Strictly speaking renewables remain in the wholesale market but the price they are paid is fixed and any revenues above the strike price paid back to the LCCC, hence to suppliers and onto consumers.

[iii] This is a function of interconnection, which tends to propagate price spikes from internationally exposed markets (such as the GB market) to those with limited domestic gas generation (such as France).