On our current trajectory, carbon emissions will increase by over 10% by 2030. This contrasts with the 43% reduction needed to limit temperature rises to 1.5°C (United Nations, 2022). Radical changes are urgently needed across society to reduce emissions and tackle climate change.

The carbon measurement problem

One challenge for speeding up decarbonisation is effective measurement. While country-level analysis is generally seen as robust, there is not currently a consistent method that provides a meaningful carbon assessment for businesses or households.

Without this information, we are blinkered to the size of our personal carbon footprints. This is likely to make both firms and individuals indecisive on the next steps to take, and it means that they lack accountability.

We therefore need more granular measures of carbon footprints, which we can aggregate up from individual businesses or households to the total footprint of the economy. Without such a system in place, it is impossible to understand the collective effort needed to make rapid reductions in emissions.

How could tagging carbon emissions help?

A promising route forward on these measurement issues may already be available. The daily economic activity of businesses and households is captured digitally, in real-time, through electronic payment data that flows between banks, suppliers and retailers.

By embedding a carbon attribute into these payments – a measure of how much carbon the underlying activity represented by the payment generates – it is possible to introduce an automated, detailed and live measure of carbon accounts. This can then, in turn, inform and drive change.

The concept of ‘carbon tagging’ draws inspiration from widely used food labelling, which informs consumers about the calorific content of food. This nutritional information prompts consumers to evaluate their choices, firms to change their ingredients and governments to take action to improve diets.

Such systems provide objective data that can create change. Carbon tagging would do the same in the equally urgent and universal challenge of emissions reduction.

The benefits from carbon tagging digital payments would extend beyond just consumer labelling. Such a scheme would introduce much needed transparency across our economies, providing a key data resource to underpin general policy interventions, such as new carbon taxation. It would also help to inform specific initiatives that could be focused on the highest emitting sectors or activities.

Does the digital technology exist to make this possible?

All key data, technology and reporting practices for carbon tagging already exist. Using data from a UK-based high street bank, it is possible to demonstrate how this process might work in practice.

Drawing on earlier research (Trendl et al, 2022), we construct a dataset of carbon multipliers – the amount of carbon produced per £1 spend on a good or service – and apply these to financial transactions from an anonymous population of 3,582,448 customers and 773,503 firms, using data on all their transactions during October 2021.

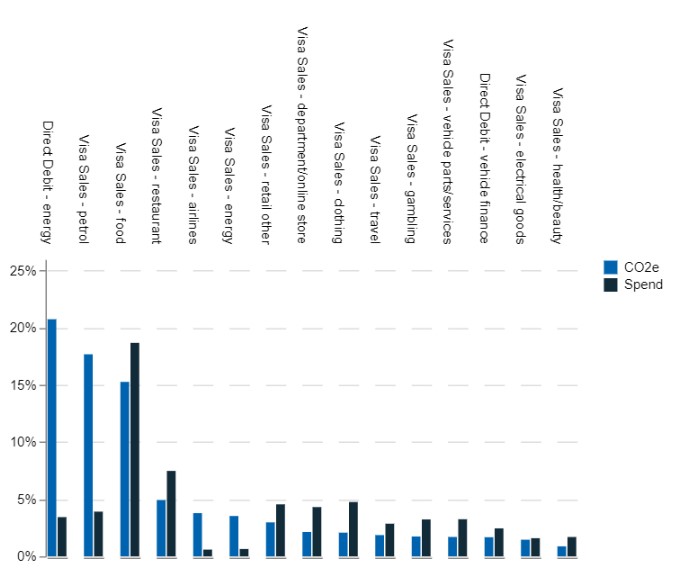

The analysis shows that emissions – when measured through digital payments – are highly concentrated in just a small number of payment types. Specifically, 15 digital payments account for almost 60% of all emissions for both individuals and households, and small and medium-sized businesses (see Figures 1 and 2).

The transactions with the highest carbon footprint are regular direct debit payments for gas and electricity, and card payments for petrol, gas and airfares. Unsurprisingly, these are carbon-intensive products and dominate household and business carbon footprints. The carbon footprints arising from purchases of food, clothing and other retail products are modest in comparison.

Figures 1-2: : Spending and emissions shares by payment category and sector (small and medium-sized businesses; households and individuals)

Source: Lloyds Banking Group personal current account and business current account records

The technology already exists to add carbon attributes to the digital payments data we see in our bank accounts and on our personal and business finance apps. Researchers have compiled ‘carbon multipliers’: key parameters that represent the emissions generated by a given unit of spending on a particular product. These rely on the continual development of multi-regional input-output analyses, which trace the flow of inputs of raw materials, and the flow of outputs of intermediate and final products through the production process (Owen et al, 2018).

For example, £1 spent on fuel has a carbon multiplier close to three – which means that 3kg of carbon are generated for each £1 spent on fuel (Kilian, 2022). Using these calculations, we can readily transform spending into corresponding carbon emissions. We should see not just the financial cost of the goods and services we buy every day measured in pounds and pence, but also the carbon cost measured in kilos and tonnes.

What are the benefits of digital carbon tagging?

For businesses, this new information could radically simplify the calculation of carbon intensities of supply chains, business strategies and, ultimately, end products. This, in turn, would empower business leaders to make informed decisions to reduce their emissions footprints.

For consumers, it would create a new, salient dimension of consumer choice. Individuals would be able to opt to change their spending patterns to reduce their own carbon footprints.

There are also important benefits for governments, as this would enable emissions to be measured at multiple levels of potential policy interventions in a consistent way. This precision would empower policy-makers to target more effective policies and learn from interventions that are working.

It would also ensure that the sum of individual parts adds up to the whole. This is currently not the case, as contemporary reporting of carbon footprints by firms tends to be inconsistent – covering different geographies, time periods and using different carbon multipliers (Giesekam et al, 2019).

What comes next?

We see three main steps to creating a new, mandatory carbon emissions attribute for those digital payments that carry the highest carbon impact.

First, an independent body needs to be established that defines the carbon multipliers, sets the standards for reporting and oversees implementation in the payments system.

This would also involve defining the scope of carbon tagging. A first generation of labelling for the most carbon-intensive forms of production and consumption should be made a priority.

Further, new policies would need to require businesses operating in sectors with high carbon intensity to carry additional responsibilities that support the tracking of emissions. With new software upgrades to payment technologies, these requirements can be automated to help to minimise the implementation burden.

For example, it would be possible to create live data feeds of carbon footprints from payments data, which could be provided in real-time to business and households, allowing them to track their carbon footprints against targets in the same way that firms might track sales or revenues.

The second key step involves engagement with payment networks to embed carbon information in digital payments alongside other existing information. The specifics of this can vary based on the particular payment type being made and other factors, such as its purpose (Bank of England, 2020).

Finally, guidance and support needs to be provided to circulate the new carbon information. This could be via reporting guidelines for bank statements, business accountancy software or data sharing for government entities and regulators.

There are already useful examples of these types of practices. For example, mandatory information disclosures are required of banks and other payments services providers when generating bank statements, and when reporting key information to tax authorities.

There is a unique opportunity to leverage our digital payment infrastructure to help society to decarbonise. This would represent a major modernisation of our approach to reaching net-zero targets.

It would ensure consistency with country-level carbon accounting while providing much needed information to government, businesses and consumers to help them make more informed choices. It would also strengthen a key requirement for our eventual success: personal accountability.